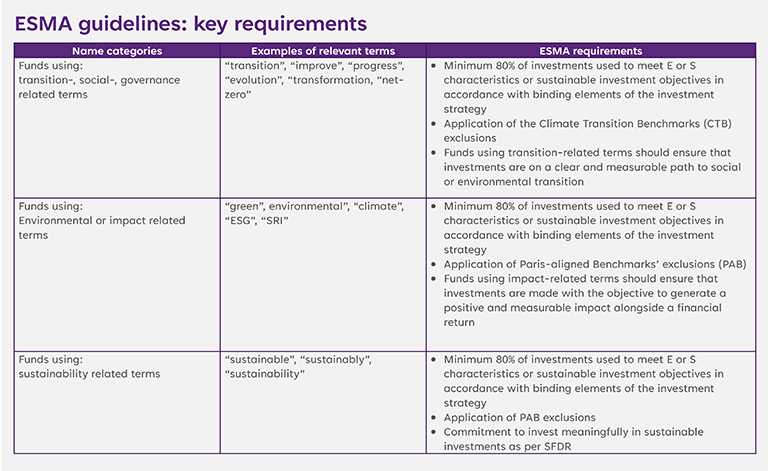

The new guidelines include several key requirements for funds using ESG- or sustainability-related language in their names.

Minimum investment threshold

Funds must invest at least 80% of their assets in line with the environmental or social characteristics or sustainable investment objectives, as defined by binding elements of their investment strategy. ESMA is not unique on this requirement. For example, in the US and UK securities markets authorities have also set similar requirements[1] [2].

Application of Paris-aligned benchmark (PAB) and climate transition benchmark (CTB) exclusions

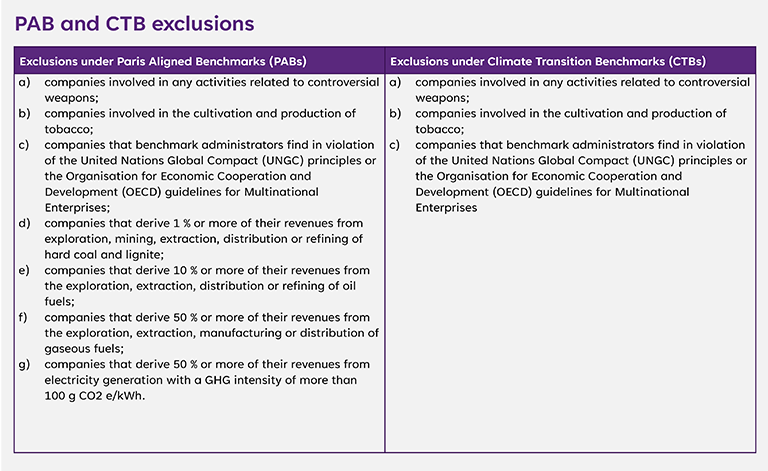

- Funds using terms like “sustainable”, “green”, “environmental”, “climate”, or “impact” must apply PAB exclusions outlined in Article 12 of the Commission Delegated Regulation 2020/1818 (see Appendix on page 4 for the list of exclusions), which was adopted in July 2020. These exclusions were initially designed to align an investment benchmark/index with the Paris Agreement goals, restricting investments in companies that derive a significant portion of their revenue from fossil fuels.

- Funds using “social” or “governance” related terms must apply CTB exclusions, noted in Article 12(1)(a) to (c) of the Commission Delegated Regulation 2020/1818 (see Appendix on page 4 for the list of exclusions).

- Funds using “transition” or related terms must apply CTB exclusions, demonstrating that their investments are on a clear and measurable path to achieving social or environmental transition.

- Funds using “sustainability” or related language must apply PAB exclusions and also invest meaningfully in sustainable investments as defined under the EU Sustainable Finance Disclosure Regulation (SFDR).

A more detailed summary is also provided as the Appendix to this article.

Triggering fund renaming or divestment

It is widely expected that the new guidelines will trigger substantial fund renaming in the market. Several research houses published their preliminary assessments of the scale. For example, Morningstar estimated that over 1,600 ESG funds would have to either change the name or drop the holdings that are incompatible with the new rules[1]. According to MSCI research, about 30% of the Article 8 and 9 funds universe could face a choice between divestments or a name change[4].

In fact, 30 Article 8 and 9 funds have already dropped ESG-related language in their names according to the most recent Q2 2024 report by Morningstar[5].

Unintended consequences and counterintuitive outcomes

Notably, the guidelines do not directly impact Article 8 and 9 fund designations under Sustainable Finance Disclosure Regulation (SFDR) – in principle, the funds would be able to keep the categorisation with or without ESG-related names. In fact, not all Article 8 or 9 funds contain sustainability-related language in their names[5]. Therefore, the market will likely continue to see a mixture of Article 8 and 9 funds that may or may not refer to ESG terms, yet likely with fewer funds being able to refer to sustainability in their names. Whilst meant to tackle greenwashing, the outcome of the guidelines may be counterintuitive in certain scenarios. For example, a hypothetical Article 8 fund called e.g. “Climate Awareness Fund”, investing in companies with carbon emissions lower than a selected benchmark, may in fact invest in companies that operate in industries that simply do not generate revenues from fossil fuels or electricity production (technology, TMT, consumer discretionary, etc) and thus would have no issues complying with the PAB exclusions. On the other hand, a hypothetical Article 9 fund (call it e.g. “Fixed Income Corporate Fund”), which is subject to more stringent requirements under SFDR and which invests in green bonds, including EUGBs[6], issued by power and utility companies financing decarbonisation or climate solutions, may not be able to use environmentally- or sustainability-related language in its name if some of the utility companies have residual fossil fuel-related business. The counterintuitive part is about the delta between the impact that the hypothetical Climate Awareness Fund and the Fixed Income Corporate Fund could generate for the transition towards a low carbon economy, and consequently about which of the two would need to attract more funding.

One can argue that the Fixed Income Corporate Fund can be called e.g. Fixed Income Net Zero Transition Fund for which investors will not need to apply the PAB exclusions, but which will need to demonstrate that investments are on a clear and measurable path to social or environmental transition. Unfortunately, the concept of a clear and measurable path to social or environmental transition has not been sufficiently defined or established, especially across differing geographic regions, and realistically it will take time for any good practice to develop and to settle in requiring consultations with legal specialists, cross-industry engagement and engagement with national regulators.

Meriting a different approach for green bonds

It appears that the ESMA guidelines may not fully recognise the role that green and sustainable bonds have been playing in attracting capital for projects contributing to environmental or/and social objectives, including the transition to a low carbon economy, as well as the process and requirements that govern the issuance of these instruments. Existing standards and frameworks, such as those produced by the International Capital Market Association (ICMA), as well as the newly adopted EU Green Bond Standard, already require issuers to demonstrate consistency between the purpose of a green bond and the wider corporate and sustainability strategy, alongside other robust requirements that have been critical to establishing credibility in this market. It may be counterintuitive again if the treatment of these instruments does not merit any exemptions or a modified regime under the ESMA guidelines.

In response to this conundrum, ICMA has provided public feedback[7] to ESMA, highlighting the potential disruption that these exclusions could cause in the green bond market. According to ICMA, the requirement to apply PAB exclusions could force many green bond funds to either rename the funds or divest from green / sustainable bonds issued by companies with some legacy fossil fuel revenues and which are actively decarbonising their activities. This would lead to substantial rebranding and restructuring within the green bond fund sector which will at the very least impose more administrative and legal costs while bringing confusion to the market. Notably, this is not the first time that investors will need to amend their fund documentation – in previous years the market saw several waves of fund re-categorisations among Article 6, 8 and 9 due to changes in legislative interpretations.

At present, green and sustainable bonds would often be held in Article 9 funds for which investors have created policies to cater for the “sustainable investment” definition under SFDR, and therefore would be subject to ‘Do No Significant Harm’ (DNSH) assessment by considering so-called Principal Adverse Impact (PAI) indicators. For green bonds, the PAI assessment can be conducted at an instrument level as opposed to at the issuer level[8]. ICMA argues that a similar approach should be applied to green bonds under the new ESMA rules where the PAB exclusions could apply at an instrument/project level and not at the issuer level. This would be a welcome approach as it would help facilitate the consistent application of interconnected regulatory regimes to the same types of instruments. This approach would also help smoothen any immediate disruption of the market or reduced liquidity, also recognising the fact that the EU SFDR itself is now due for a revision[9] and which may require further adjustments to how investors run and market ESG funds in the future given the potential introduction of distinct labels for ESG/sustainability funds. Finally, it would provide corporate issuers with certainty and reassurance that their efforts to issue green and sustainable debt to support environmental and social transition is supported as opposed to being unduly penalised.